What Is Open Banking? – A Breakthrough in External Connectivity for Banks

What is Open Banking? – Advancing External Connectivity in Banking Operations

The origins of Open Banking lie in the long-standing, closed operating model of the traditional banking sector—where data and customer interactions were tightly controlled within institutional boundaries. Customer data was treated as a proprietary asset, stored in isolated internal systems. However, in the digital era, data only realizes its true value when it is actively leveraged to expand product offerings and enable meaningful connections beyond the bank’s own ecosystem.

Open Banking represents a financial model that allows banks to share customer financial data with third parties—such as fintech companies and service providers—through Application Programming Interfaces (APIs).

This model enables banks to extend their reach beyond traditional channels, unlocking new customer segments and service opportunities. In this context, Artificial Intelligence (AI) plays a pivotal role. AI processes vast streams of data, continuously learning, analyzing, and generating real-time insights. These capabilities enhance the efficiency of financial service delivery while enabling banks to engage and acquire customers more effectively in the digital landscape.

How AI Is Reshaping Open Banking

Artificial Intelligence (AI) is rapidly transforming the Open Banking landscape, enabling more intelligent, data-driven financial services. Its applications are becoming increasingly widespread and impactful:

- Hyper-personalization: Gone are the days of mass marketing emails. By analyzing transaction histories across multiple banks, AI can deliver highly tailored financial recommendations for each individual customer. For instance, if a customer consistently overspends, AI can go beyond simple alerts—proactively suggesting automated savings plans or allocating funds into flexible investment portfolios.

- Enhanced credit scoring: AI leverages data from Open Banking sources—such as utility bills, shopping behavior, and e-wallet payment histories—to build alternative credit profiles. This enables financial institutions to assess individuals who lack traditional credit histories, significantly expanding access to financial services and promoting greater financial inclusion.

- Proactive risk management: Rather than detecting fraud after the fact, AI enables real-time identification of anomalous behaviors and potentially fraudulent transactions. It can trigger instant alerts or even support automated decision-making, allowing banks to block suspicious activities at the moment they occur.

Banks are transforming the way they interact with external partners

In this model, banks are no longer the endpoint of services but instead function as a platform. The interaction between banks and external partners—Third-Party Providers (TPPs)—is increasingly expanding:

- Banks are enabling third-party applications to perform tasks that traditionally required direct customer interaction, such as initiating payments directly from bank accounts, bypassing intermediary steps like credit cards.

- They also allow applications to aggregate data from multiple accounts to provide a comprehensive view of customers’ financial situations.

Modern banks are proactively building integration gateways, where Fintech companies and external partners can seamlessly connect their services, creating a symbiotic ecosystem that continuously expands and delivers financial services to new customer segments.

Benefits of Open Banking

Open Banking frees customers from being tied to a single bank. They can manage their entire financial life through a single application, access more affordable financial products thanks to increased competition, and enjoy a user experience optimized at every touchpoint.

For banks, Open Banking enables customer base expansion without the need to invest in additional physical branches. More importantly, it unlocks new revenue streams through Banking-as-a-Service (BaaS). Banks can charge fees per API call or collaborate with fintech partners to develop niche financial products with high growth potential.

Challenges in Expanding Open Banking

Despite its strong potential, the implementation of Open Banking—especially when combined with AI—faces several inherent challenges:

- Security and Privacy: This remains a primary concern. Opening up data increases exposure to cyberattacks and fraud in digital environments. Furthermore, applying AI to sensitive financial data requires robust regulatory frameworks to prevent misuse and ensure compliance with legal standards.

- Legacy Systems: Many banks continue to operate on outdated technology platforms built decades ago. Integrating modern APIs into these complex and rigid systems presents significant challenges in both cost and human resources.

- Trust Barriers: Customers remain cautious about sharing passwords or granting account access to third parties. Building trust is a long-term process that requires transparency and strong security assurances.

Opportunities for Technology and Fintech Companies

In this evolving landscape, technology firms are not merely partners—they are key enablers shaping the future of Open Banking:

- Connectivity Infrastructure: There is strong demand for middleware platforms that standardize APIs between banks and external partners, making this a highly promising segment.

- Specialized AI Solutions: Developing AI models tailored specifically for Open Banking data—such as transaction classification or cash flow forecasting for SMEs—offers significant value.

- Embedded Finance: Open Banking creates opportunities to integrate financial services into everyday applications—from retail and healthcare to education—by leveraging APIs and AI capabilities.

Open Banking and AI are reshaping the global financial landscape. Success will not belong to the largest institutions, but to the fastest and most adaptable—those capable of building seamless connections and deeply understanding customer needs.

As regulatory barriers gradually ease and AI becomes more accessible, financial services are increasingly integrated into daily life—delivered in smarter, more intuitive ways than ever before.

This article is an exclusive contribution by Luong Ngoc Binh, Digital Technology – Data – AI Expert in the Banking and Financial Services sector.

With over 16 years of experience in finance and banking, including more than 10 years in digital banking, he specializes in consulting and developing Data–AI solutions for financial institutions. He has contributed to the development of core platforms and digital solutions for major banks such as BIDV, Agribank, and PVCombank.

References

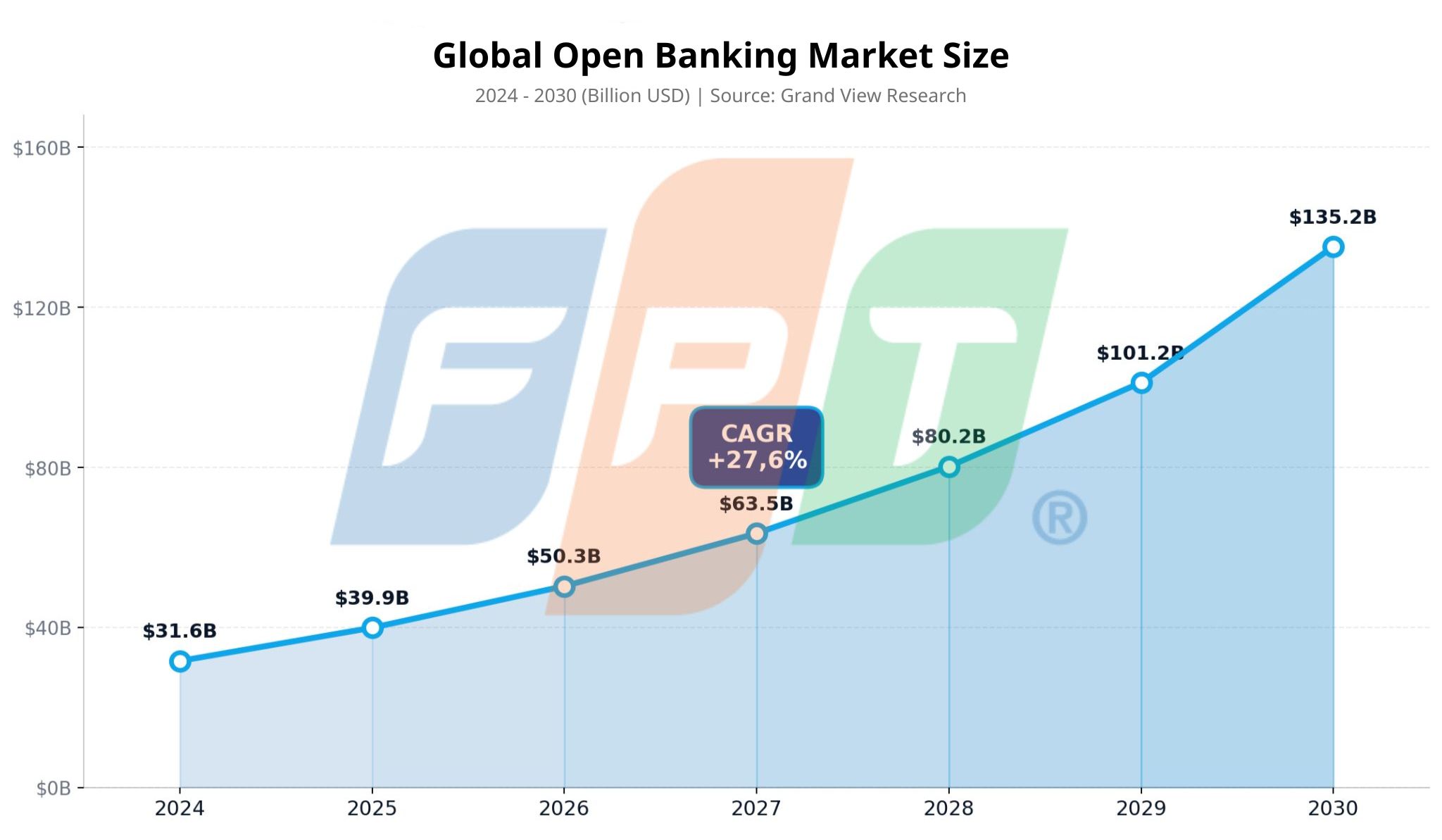

[1] Grand View Research (2024). Open Banking Market Size, Share & Trends Analysis Report, 2025–2030.

[2] Grand View Research – Press Release (2024). Open Banking Market Size To Reach $135.17 Billion By 2030.

[3] Grand View Research – Europe Outlook (2025). Europe Open Banking Market Size & Outlook, 2030.

[4] Feedzai (May 2025). 2025 AI Trends in Fraud and Financial Crime Prevention.

[5] Feedzai (2025). State of AI in Financial Crime Prevention.

[6] Business Wire (May 6, 2025). Feedzai: More Than 50% of Fraud Driven by AI and Hyper-Realistic Impersonations.

[7] Coinlaw.io (2024).Online Banking Usage Statistics 2025

[8] Open Banking Limited (May 2025). Impact Report 7. Open Banking delivers real-world impact as adoption accelerates year-on-year

[9] Open Banking Limited (September 2025). 2 Billion API Calls and 15 Million Users. 2 Billion API calls and 15 Million users — a landmark month for open banking in the UK.

[10] Open Banking Limited (January 2026). Open Banking in 2025: Now Part of the UK’s Everyday Financial Life.

[11] Juniper Research (April 2025). Open Banking User Numbers to Surge by Over 250% by 2029.

[12] AWISEE (2025). Neobanking Statistics: Market Size, Users & Growth Trends.