How should businesses report emissions within scopes 1, 2, and 3?

Overview:

Reporting emissions not only contributes to businesses creating positive societal values and avoiding legal risks but also helps them keep up with the green transformation trend and rapidly expand market share as the global “green supplier” race unfolds. To achieve this, understanding how to report emissions within Scopes 1, 2, and 3 as stipulated by the GHG Protocol is essential.

1. How are the top 1,000 largest businesses in the world transitioning towards sustainability?

Professor Michael E. Porter and Forest L. Reinhardt at Harvard University emphasize:

“If businesses continue to treat climate change as something nice to be done rather than a new business threat, they will face the most severe consequences in the future”.

![]()

(Net Zero Tracker, 2023)

According to Accenture (2023), currently more than 50% of the top 1,000 largest companies in the world have committed to achieving Net Zero targets by 2050. Data from the Net Zero Tracker (2023) shows that the world’s largest capitalized companies across all sectors, such as Walmart, Apple, Amazon, and Volkswagen, have all joined the Net Zero race. Many of these companies are expected to reduce emissions to net zero by 2025. The table above also outlines their implementation roadmap as follows:

- Emissions Reporting Mechanism: This is the first step of the Net Zero journey. Companies need to understand how much emissions they currently emit, from buildings to core business operations…

- Detailed Emissions Reduction Strategy: After identifying the main contributors to emissions, companies need to develop strategies and actions to reduce emissions. For example, Amazon uses electric vehicles for transportation, replaces plastic packaging with paper, uses 100% recyclable packaging, and fulfillment centers powered by solar energy. Apple requires 100% of their component suppliers (including those in Vietnam) to use renewable energy in the manufacturing process. The phone components use aluminum and are recyclable. Companies like Mercedes, BMW, and Volkswagen are transitioning to electric or hybrid vehicles. For gasoline cars, they are working on improving technology to reduce emissions from 200 g CO2/km to 50 g/km to meet EU Taxonomy standards.

- Net Zero Target Identification: This is a big question for investors, governments, and stakeholders concerning businesses. After having a clear strategy, plan, and actions, companies need to estimate the time to achieve carbon neutrality.

- Carbon Credit Purchase: For industries where achieving carbon neutrality is particularly challenging, such as Exxon Mobil in the fuel industry, companies need to purchase additional carbon credits. For example, an Exxon Mobil plant emits 160,000 tons of CO2 (tCO2e) per year and has no other way to minimize emissions. Knowing that each hectare of mangrove forest will generate 16 carbon credits (equivalent to absorbing 16 tons of carbon annually). Thus, Exxon Mobile needs to purchase an additional 160,000 carbon credits from 10,000 hectares of mangrove forest at a price of $30 per credit. The total annual cost to offset carbon is $4.8 million (equivalent to 110 billion Vietnamese dong).

- Scope 3 Reporting: Scope 3 is part of emissions reporting, accounting for over 80% of a company’s total emissions. However, Scope 3 is very difficult to accurately estimate and requires highly skilled personnel in the field of Climate Change.

This article will help businesses understand how to disaggregate their emissions into scopes 1, 2, and 3 to keep up with the green transformation trend and the sustainable development of the world.

2. What is the GHG Protocol?

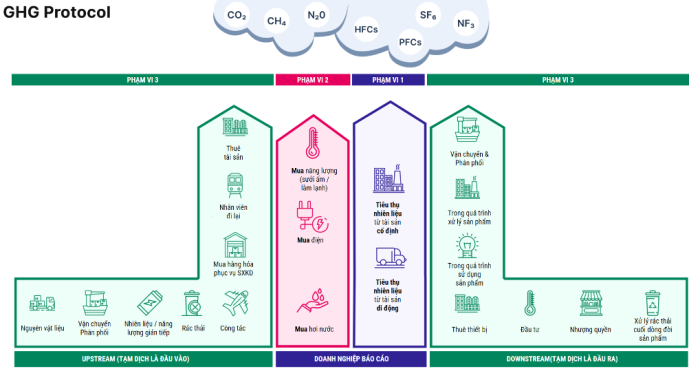

The GHG Protocol is an international guidance developed by the World Business Council for Sustainable Development and the World Resources Institute. Currently, the GHG Protocol provides standards and guidelines for specific emission calculations and is adhered to by the majority of businesses worldwide. According to the GHG Protocol, emissions are divided into 3 scopes:

- Scope 1 (Direct emissions): Emissions directly generated from the combustion of fuels by assets owned or controlled by the company. Examples include emissions from fuel combustion in factories, furnaces, or other equipment owned or controlled by the company.

- Scope 2 (Indirect emissions): Indirect emissions from the PURCHASE OF ENERGY from third parties. Unlike direct emissions (which are included in scope 1), emissions from scope 2 DO NOT OCCUR at assets owned by the company but indirectly associated. For example, a company in the agriculture sector consumes 5,000 MWh of electricity annually for lighting and heating for livestock. Before these 5,000 MWh are transmitted to the grid, at ABC Thermal Power Company, they have to burn 7,407 tons of coal and generate emissions. Thus, because the company is the buyer and user of electricity, according to the GHG Protocol, the company is responsible for these emissions.

- Scope 3 (Other indirect emissions): Other indirect emissions created throughout the entire value chain but not owned or controlled by the organization. Types of scope 3 emissions include emissions from business travel, transportation and distribution activities, the use and disposal of products, and emissions associated with employee commuting. Scope 3 emissions are the most complex to calculate but account for over 80% of total emissions.

Description of Scope 1, 2, and 3

3. Reporting Scope 1 Emissions

Scope 1 emissions are direct emissions generated from the combustion of fuels by assets owned or controlled by the company. The components of Scope 1 include:

- Fixed combustion: Includes all emissions from fuel combustion in factories, furnaces, or other equipment owned or controlled by the company.

- Mobile combustion: Includes all emissions from company-owned or controlled transportation vehicles, such as cars, trucks, and vans.

- Leakage emissions: Include greenhouse gas emissions leaked from equipment, such as air conditioners and refrigerators. Note that greenhouse gas emissions from these devices can be thousands of times more hazardous than CO2. Companies are encouraged to report these types of emissions.

To illustrate, we will use the example of emissions disaggregation in Scope 1 for a steel industry business. Steel companies are one of the largest greenhouse gas emitting industries globally. Scope 1 emissions from steel companies mainly come from the combustion of fossil fuels to smelt iron ore and produce steel.

Illustration of the steel production process (Industry Transition, 2021)

Types of greenhouse gases emitted from steel companies include:

- Carbon dioxide (CO2): CO2 is the primary greenhouse gas emitted by steel companies. CO2 is generated when fossil fuels, such as coal, natural gas, or oil, are burned to provide heat for the steel production process.

- Methane (CH4): CH4 is a greenhouse gas more potent than CO2. CH4 is produced in the steel production process from various sources, such as incomplete combustion of fossil fuels, fermentation process, and wastewater treatment.

- Nitrogen oxide (NOx) / Sulfur dioxide (SO2): NOx and SO2 are air pollutants that can contribute to the greenhouse effect. NOx is generated in the process of burning fossil fuels to provide heat for the steel production process.

Here is another example of Scope 1 emissions reporting in the software industry:

Microsoft’s Scope 1 Emissions Report for 2020-2022

To simplify reporting Scope 1 emissions, businesses can review all production activities, assets owned or controlled by the company (financially or operationally), and then quantify the amount of fuel from which total emissions can be estimated to come from Scope 1.

Illustration of Microsoft’s Data Center (CNET, 2023)

4. Reporting Greenhouse Gas Emissions: Scope 2

Scope 2 emissions refer to the indirect emissions resulting from the purchase of energy from third parties. Unlike direct emissions (which fall under Scope 1), emissions from Scope 2 do not occur at the assets owned by the entity but rather indirectly associated with them. For instance, a real estate company owning multiple office buildings annually consumes 2,000 MWh of electricity for lighting and air conditioning. Before this electricity is transmitted into the grid, at the ABC Power Plant, they have to burn 7,407 tons of coal, resulting in greenhouse gas emissions. Therefore, as the entity is the purchaser and user of electricity, according to the GHG Protocol, it is responsible for these emissions.

Illustration of a coal-fired power plant (Vietnamnet, 2023).

In Scope 2, electricity consumption is usually the primary source, but there are two other sources:

- Purchased heating and cooling systems

- Purchased steam

For small or medium-sized enterprises, or those without the need for year-round heating, cooling, or steam systems, they may purchase these from third parties. According to the GHG Protocol, because the entity is the purchaser and the emissions occur indirectly and not at assets owned by the entity, they need to be reported within Scope 2.

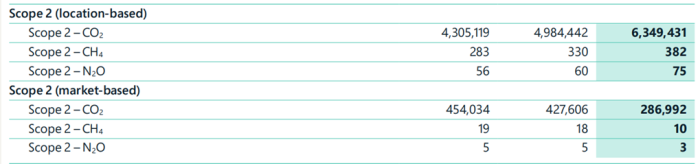

Example of Microsoft’s Scope 2 Emissions Reporting from 2020-2022

In Scope 2, there are two methods for converting electrical energy (MWh) into CO2 emissions, namely market-based and location-based.

- Market-based: It is calculated based on the emission factor provided by the electricity supplier.

- Location-based: It is calculated based on the emission factor for each country or territory.

To accurately choose the appropriate method according to the requirements of each country, businesses need to have a clear understanding of the regulations of the respective countries where they have offices/headquarters/plants located.

5. Reporting Greenhouse Gas Emissions: Scope 3

Scope 3 emissions encompass all other indirect emissions generated across the entire value chain but not owned or controlled by the organization. Types of Scope 3 emissions include:

- Emissions from business travel and commuting: For example, a textile company with 20,000 employees commuting monthly. Annually, upper management takes a total of 1,500 domestic and international flights and stays an average of 3 nights in hotels. Thus, the textile company needs to report emissions for all travel, movement, and work performed by employees.

- Emissions from the production, transport, and purchase of raw materials: For example, a plastics manufacturing company will have Scope 3 emissions from oil and gas extraction for producing virgin plastics, as well as from transporting raw materials to the company’s facilities.

- Emissions from transportation and distribution activities: For example, an automobile manufacturing company will have Scope 3 emissions from transporting cars to retailers, as well as from delivering cars to end consumers.

- Emissions from the use and disposal of waste: For example, an electronics company will have Scope 3 emissions from using batteries and other electronic products, as well as from the disposal of electronic waste.

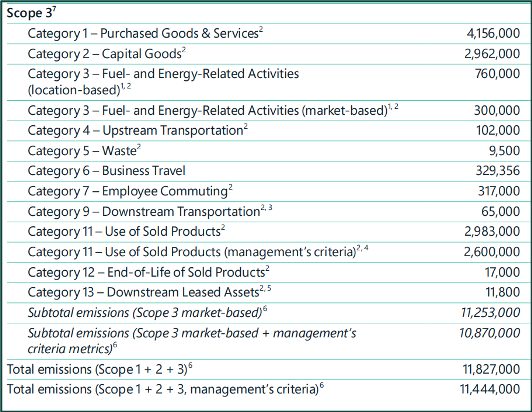

An example of Microsoft’s Scope 3 emissions report for 2022.

Reporting Scope 3 emissions is the most complex process defined by the GHG Protocol, but it accounts for over 80% of emissions.

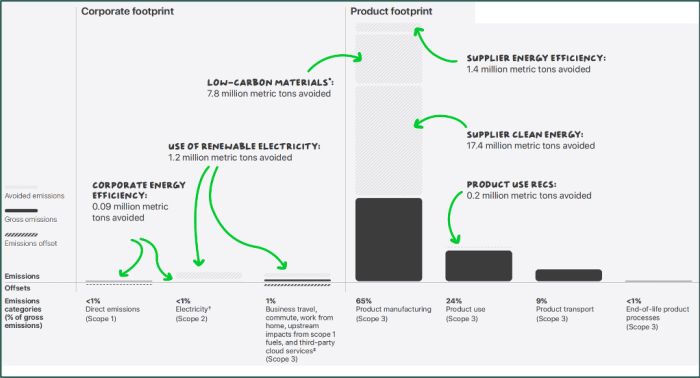

The emission intensity by scope for Apple in 2022 (Apple, 2022).

According to current regulations in Vietnam and globally, organizations are required to report emissions within Scope 1 and 2. However, leading global companies have already begun reporting Scope 3 emissions due to increasing demands from investors and stakeholders. Scope 3 is expected to create fierce global competition for green suppliers. In the latest report by Oracle (2022), they aim to have 100% of their suppliers report emissions and use green electricity. In the seafood industry, in the second half of 2023, there was a yellow card due to major retail chains in Europe also starting to demand suppliers in Vietnam to have sustainability certifications.

Thus, greenhouse gas reporting not only contributes to organizations building positive societal values and avoiding legal risks but also helps organizations keep up with the green transformation trend and quickly expand market share as the “green supplier” race unfolds globally.

Exclusive article by FPT IS Technology Expert

Pham Tuan

VertZéro Product Manager

FPT Information System Company.