Personalized wealth management: A tailored suit with precision craftsmanship

Two customers walk into the same bank, yet receive entirely different services. The first, a 38-year-old doctor with USD 200,000 in savings, aims to invest most of their monthly income to fund their child’s education and prepare for retirement. The second, a 52-year-old entrepreneur with USD 8 million in assets, requires advisory on intergenerational wealth transfer, cross-border tax optimization, and access to a Private Equity fund approaching its Pre-IPO phase.

Both are valuable clients. But if the bank offers them the same products and service model, one or both will inevitably leave for a competitor that better aligns with their needs. This is why the global wealth management industry is fundamentally restructuring its service approach around a core principle: segment-based personalization.

Read more related articles: https://fpt-is.com/goc-nhin-so/cau-truc-nen-tang-wealth-tech-hien-dai/

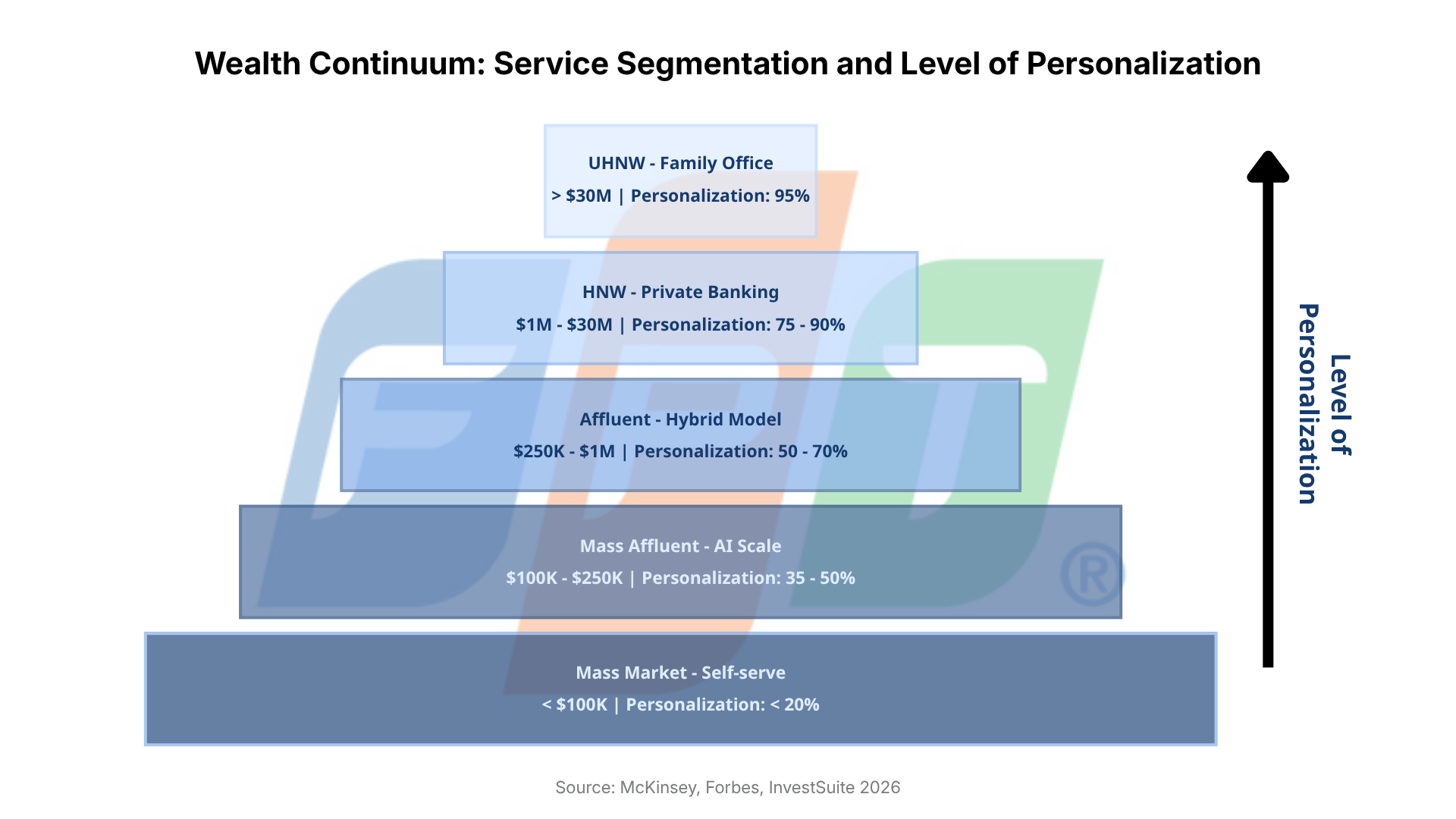

Figure 1: The Wealth Continuum Model – Levels of personalization increase with asset size.

1. Wealth Continuum – A layered view of wealth management

The global wealth management industry operates along a value chain known as the Wealth Continuum, where each asset tier is served through a distinct service model. The differentiation goes beyond account balances, it reflects financial goals, investment behaviors, risk complexity, and expectations of the client–institution relationship.

According to global data from 2025-2026, the Mass Affluent segment – clients with investable assets between USD 100,000 and USD 1 million – holds approximately USD 83 trillion, accounting for 40% of global personal wealth, with a projected CAGR of 5.4% through 2028. Meanwhile, the HNW (High Net Worth, USD 1-30 million) and UHNW (Ultra High Net Worth, above USD 30 million) segments collectively manage USD 90.5 trillion – surpassing even the affluent middle class. These are two massive markets, yet they cannot be served with a one-size-fits-all model.

Why can’t a single service model fit both?

The answer lies not only in asset size. Mass Affluent clients typically focus on clearly defined, time-bound goals – such as buying a home, building retirement savings, or ensuring family financial security. They prioritize clarity, convenience, and the ability to self-manage portfolios via digital platforms with minimal reliance on advisors. In contrast, HNW clients operate within complex financial ecosystems involving multiple asset classes, cross-border risks, and multi-generational wealth structures – requiring multidisciplinary advisory teams to design highly customized strategies, akin to tailoring a bespoke suit.

2. Personalization at scale: Serving the Mass Affluent segment

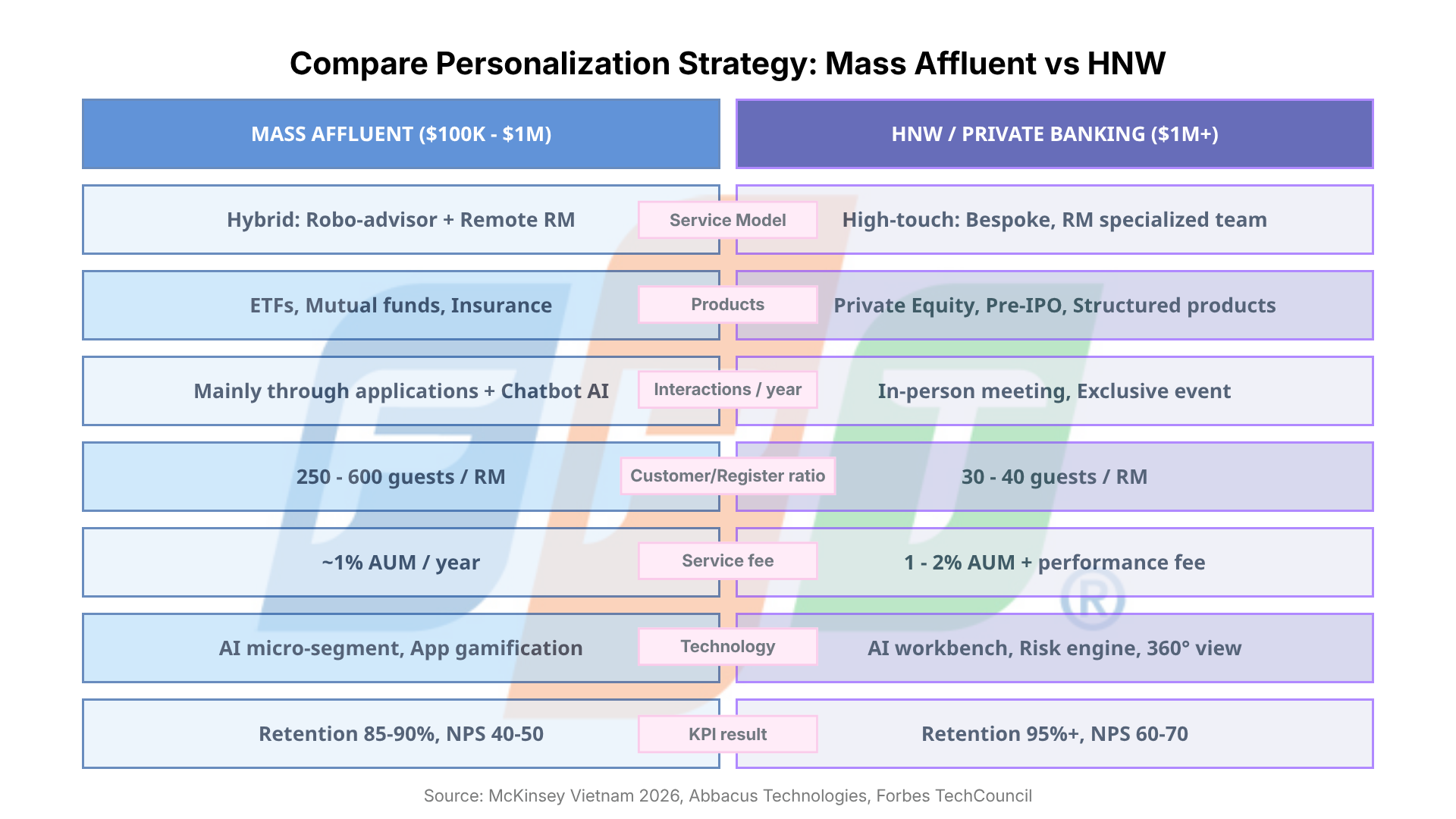

The core challenge in serving Mass Affluent clients lies in economics. With advisory fees averaging around 1% of AUM annually, a client with USD 200,000 generates only USD 2,000 in revenue. The traditional one-to-one advisory model – where each Relationship Manager (RM) handles 40-50 clients – is no longer cost-effective. This is why “hyper-personalization at scale” has become a strategic imperative across the industry.

This model operates across four layers:

First, AI and machine learning segment the customer base into 20+ micro-segments – not just by age and income, but also by personal values, life goals, risk appetite, and spending behavior.

Second, automated goal-tracking systems continuously learn from individual behavior and dynamically adjust investment recommendations in real time.

Third, platforms such as InvestSuite’s Portfolio Optimizer can process millions of portfolio optimizations daily – enabling each client to receive a fully personalized portfolio with features such as ESG filtering, goal-based investing, and tax-loss harvesting.

Fourth, human advisors are not eliminated – they are repositioned. Instead of administrative tasks, RMs focus on clients nearing the USD 1 million AUM threshold and on critical life events that require human engagement.

The result: a single RM can manage 250-600 clients instead of 30-40 under the traditional model, while maintaining sufficient personalization to sustain retention rates of 85-90%.

Figure 2: Comprehensive comparison of personalization strategies between Mass Affluent and HNW

3. Bespoke Banking: The art of serving HNW clients

If Mass Affluent requires personalization at scale, HNW clients demand the opposite: high-touch, non-scalable, deeply bespoke service. This is the essence of bespoke banking, where the boundary between investment management and life management becomes increasingly blurred.

A typical HNW client does not simply seek stock recommendations. They expect their bank to understand that they are considering real estate investments in Europe, that their children may study in the UK, and that their family business could go public within three years. Every financial recommendation – investment strategy, trust structuring, tax planning, and estate planning – must align with this broader context. McKinsey refers to this as a “holistic advisory framework”, which distinguishes true Private Banking from standard premium investment services.

Technology still plays a critical role, but differently. Instead of directly serving end-users, it empowers RMs. An AI Workbench can aggregate transaction histories, risk behaviors, and market intelligence to generate complex investment strategies within minutes – allowing RMs to focus on what technology cannot replace: building trust and long-term relationships.

In the HNW segment, success is measured not only by return on investment. Retention rates must exceed 95%, Net Promoter Scores (NPS) range between 60-70, and cross-sell ratios reach 5-7 products per client, nearly double that of the Mass Affluent segment. These metrics reflect the deep trust and engagement enabled by bespoke service models.

4. Vietnam’s Opportunity: A USD 600 billion wealth market in the making

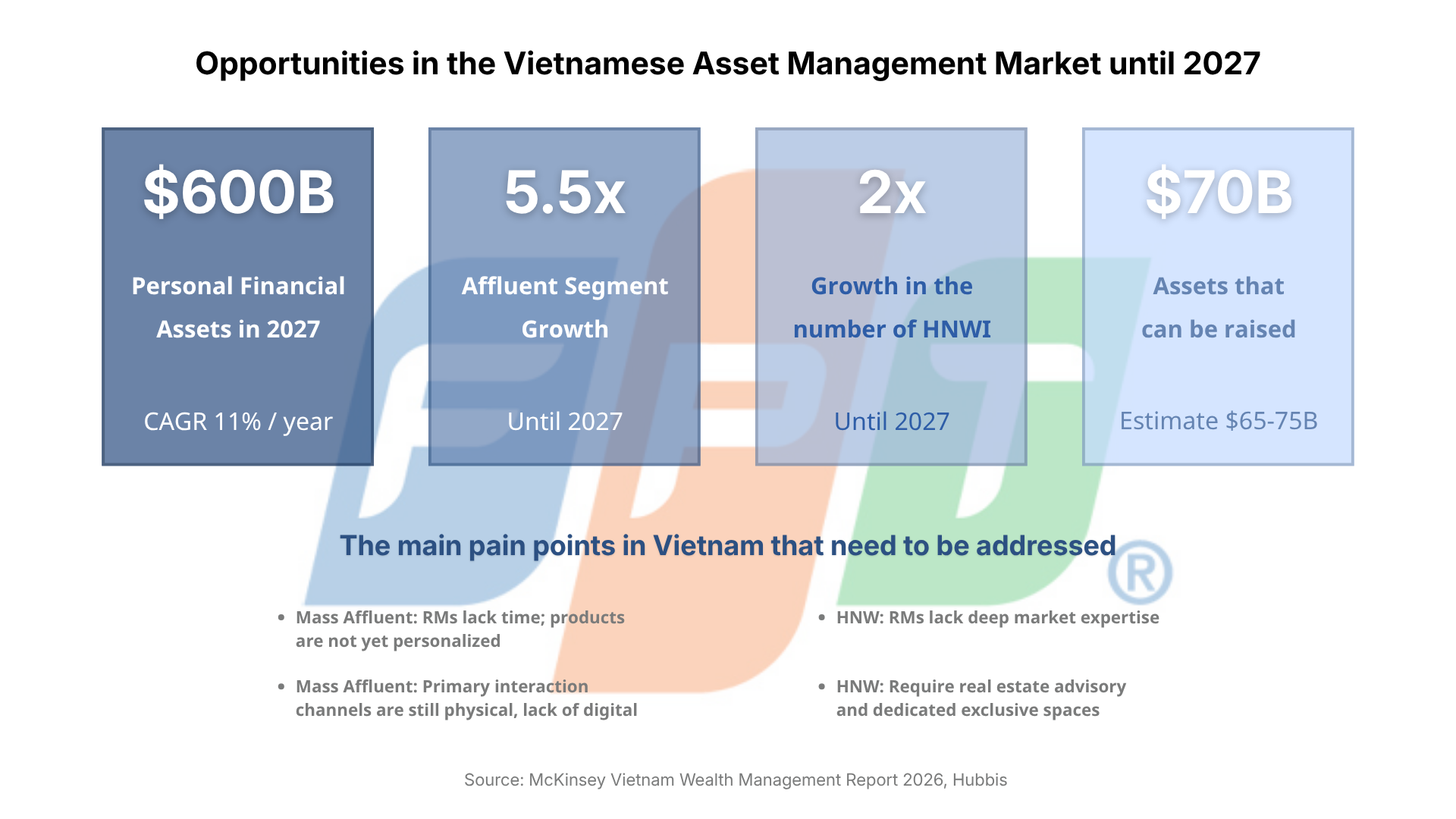

Figure 3: Wealth market opportunities in Vietnam up to 2027

Vietnam is on the cusp of a major wealth transformation. According to McKinsey, total personal wealth could reach USD 600 billion by 2027, growing at a CAGR of 11% – one of the fastest rates in the region. The Affluent segment is projected to expand 5.5 times, while the number of HNW individuals is expected to double. The opportunity from under-managed wealth is estimated at USD 65-75 billion.

However, Vietnam presents unique challenges that complicate personalization strategies. McKinsey surveys highlight key pain points among Mass Affluent clients: RMs lack sufficient time to deliver quality service, product offerings lack differentiation, and interaction channels remain largely offline – despite growing demand for seamless digital experiences among younger clients. For HNW clients, challenges are equally significant: RMs often lack deep domain expertise, particularly in real estate advisory and complex financial structuring, and clients place high value on private, exclusive environments for discussing personal wealth matters.

This is why McKinsey emphasizes: “Technology is the second enabler – but wealth platforms must be designed separately for each segment.” A single platform cannot simultaneously serve app-based users seeking portfolio autonomy and clients requiring multi-generational family office dashboards.

5. Wealth Technology: An enabler, not a replacement

A recurring question in the industry is whether AI and automation will replace Relationship Managers. In practice, the answer is no, but the role is evolving significantly.

For Mass Affluent clients, technology handles most operational tasks: suitability screening, portfolio construction, automated rebalancing, goal tracking, and proactive communication via digital channels. RMs become orchestrators – intervening at key asset thresholds or life events. This model enables one RM to effectively serve hundreds of clients without compromising quality.

For HNW clients, AI operates behind the scenes: aggregating 360-degree data views, running risk models, identifying alternative investment opportunities, and supporting RM preparation with deep analytical insights. Meanwhile, RMs focus on what matters most: listening, understanding, and building trust that cannot be digitized.

This represents an optimal division of labor between artificial intelligence and emotional intelligence. Financial institutions that master this balance will gain a sustainable competitive advantage in the decade ahead.

Conclusion

Segment-based personalization in wealth management is not a passing trend – it is a structural shift in how the financial industry creates value. When USD 100,000 and USD 10 million raise fundamentally different questions about finance, life, and legacy, the answers must be equally differentiated.

Winning institutions will not be those that serve a single segment best, but those capable of designing a seamless journey, where today’s Mass Affluent client becomes tomorrow’s HNW client, and each stage is supported with the appropriate level of personalization.

This is the true definition of the Wealth Continuum – not merely a segmentation framework, but a commitment to accompany clients throughout every stage of their financial journey.

| Exclusive article by Mr. Le Thanh Hai – Digital Technology, Data & AI expert in banking and finance

With over 15 years of experience in the banking and financial sector, Mr. Le Thanh Hai has collaborated with leading global partners such as IBM, Oracle, AWS, Microsoft, and Fujitsu. He specializes in consulting Data and AI solutions for financial institutions, contributing to the development of core banking platforms in Japan and Vietnam, and has been directly involved in building payment card systems for SHB Bank. |

References

- McKinsey & Company. “Wealth Management in Vietnam: A $600 Billion Wealth Market by 2027.” mckinsey.com/vn

- Forbes Technology Council. “How AI Hyper-Personalization Can Transform Wealth Management in the Mass Affluent Segment.” forbes.com (2025)

- Temenos. “Mass Affluent Momentum.” temenos.com/blog

- InvestSuite. “Top Wealth Management Trends in 2026: The Shift to Agentic AI and Private Markets.” investsuite.com

- Hubbis. “Vietnam’s Dynamic and Growing Wealth Management Market.” hubbis.com

- Abbacus Technologies. “Tiered Advisory WealthTech Platform.” abbacustechnologies.com