AI-powered A/B testing: When digital banking moves from “experimentation” to “continuous optimization”

Imagine a digital bank simultaneously running 200 different onboarding screen variations – each tailored to a specific customer segment, time of day, and device type. No team is large enough to manage such complexity manually. With AI, however, this is no longer a distant vision; it is how leading banks are optimizing customer experiences today.

AI-powered A/B testing at scale represents a fundamental shift from running occasional experiments to operating a continuous optimization engine for digital banking. This article explores what it is, why banks need it, who is doing it well, and how to implement it effectively.

Traditional A/B testing is reaching its limits

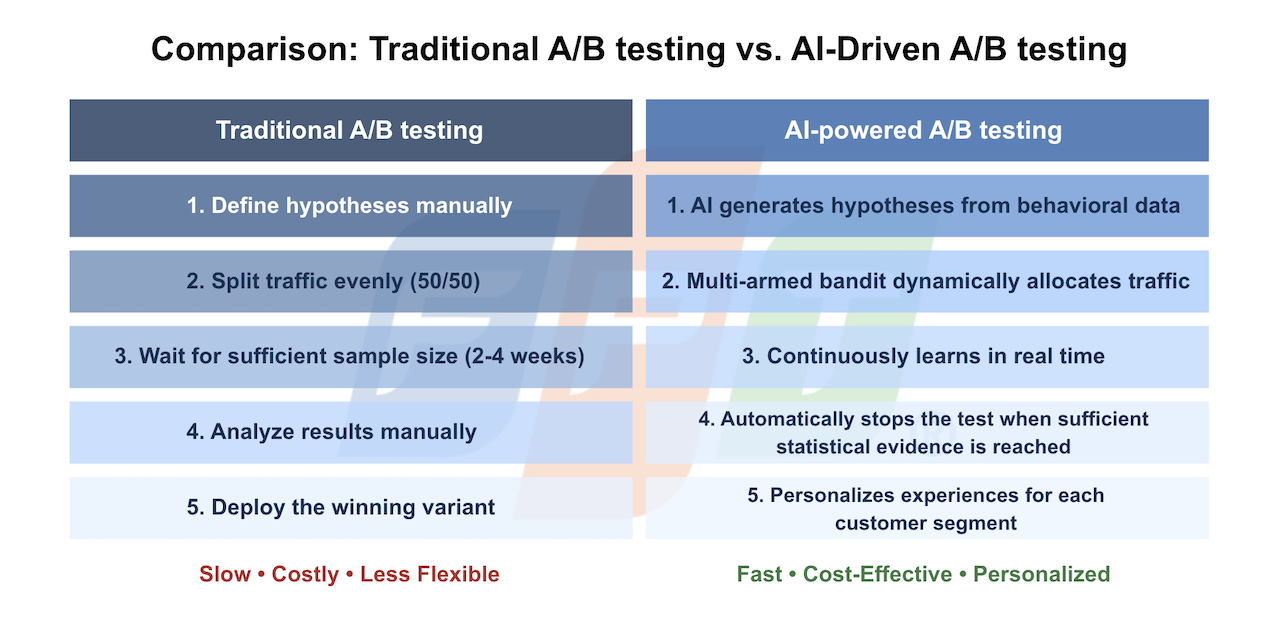

For years, traditional A/B testing has been the standard tool for product and growth teams: select two variants, split traffic evenly at 50/50, wait two to four weeks for a statistically significant sample size, analyze the results, and deploy the winning version. This model works well when applications are relatively simple, customer populations are homogeneous, and user behavior remains stable.

Digital banking, however, operates under none of these conditions. Customer behavior changes with seasons, market events, demographics, and even emotional states. An eKYC campaign that performs exceptionally well in January may generate entirely different results in July. Every day involves dozens of customer journeys – from opening a new account and activating a card to applying for consumer loans and configuring payment limits. Running sequential A/B tests manually across each of these workflows is simply not scalable.

Figure 1. Traditional A/B testing vs. AI-powered experimentation

Figure 1. Traditional A/B testing vs. AI-powered experimentation

What can AI do that humans cannot?

When AI is integrated into the experimentation process, three core capabilities emerge.

First, AI can predict which variation is most likely to outperform others based on historical behavioral data. This allows low-performing alternatives to be eliminated early, rather than waiting for statistical significance to be reached.

Second, through multi-armed bandit algorithms, the system dynamically adjusts traffic allocation while the experiment is still running. Instead of maintaining a fixed 50/50 split, traffic is progressively directed toward better-performing variants. This significantly reduces the cost of exposing customers to underperforming experiences. Research from Stanford Graduate School of Business indicates that adaptive experimentation models can reduce decision-making time by 40-60% compared to traditional static split testing.

Third, AI automatically identifies behavioral patterns across customer segments that would be difficult for humans to detect manually. For example, customers aged 25-35 in urban areas may respond better to conversational onboarding experiences, while customers aged 45 and above may prefer traditional interfaces with more detailed information. When this level of personalization is automated at scale, it becomes a genuine source of competitive advantage.

“This is no longer a marketing challenge. It is about building an organizational capability to learn from customers faster than competitors and sustaining that advantage over time.”

Where are banks applying AI-powered experimentation?

The range of applications is far broader than many realize.

In onboarding and eKYC journeys, banks experiment with step sequencing, document submission flows, instructional language, and verification waiting times. A seemingly minor adjustment to identity verification prompts can improve onboarding completion rates by 15-20%.

In upsell and cross-sell initiatives, AI evaluates the timing of loan offers, displayed interest rates, product benefit messaging, and call-to-action strategies. According to the IBM Institute for Business Value, AI-leading banks have achieved 30-45% higher conversion rates in personal lending campaigns by combining personalization with systematic experimentation.

Another less-discussed but highly important use case is fraud detection optimization. Banks can test different fraud alert thresholds to reduce false positives, legitimate transactions that are incorrectly blocked, without increasing actual fraud rates. This balancing act requires continuous experimentation and data-driven optimization rather than manual rule tuning.

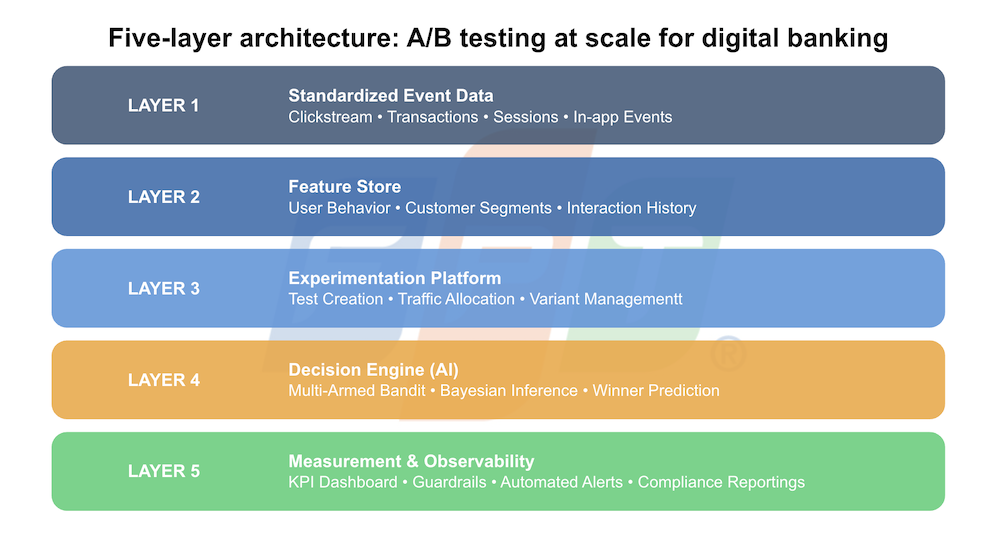

The operating architecture: Five essential layers

A scalable A/B testing capability is not a single tool, it is a coordinated technology stack composed of five tightly integrated layers.

Figure 2. Five-layer architecture for A/B testing at scale in digital banking

Figure 2. Five-layer architecture for A/B testing at scale in digital banking

The event data layer serves as the foundation. Every click, scroll, transaction, and session must be captured consistently using standardized schemas. The feature store aggregates and computes real-time behavioral attributes for each customer. The experimentation platform manages test creation, traffic allocation, and variation control. The AI decision layer, typically combining multi-armed bandit algorithms with Bayesian inference, drives continuous optimization. Finally, the observability layer monitors KPIs, guardrails, and automated alerts whenever abnormal behavior is detected.

One critical architectural principle is the separation of traffic by product line, risk segment, and customer lifecycle stage. Without this separation, experiments can interfere with one another. For example, a test targeting new customers may inadvertently impact results for loyal customers, leading to distorted conclusions and unreliable insights.

Risk governance: What banks cannot afford to ignore

Unlike e-commerce or media organizations, banks operate under stringent regulatory oversight and carry significantly higher responsibilities toward customers. Any AI model deployed within banking must incorporate governance, explainability, and regulatory compliance, and experimentation platforms are no exception.

Three common risks emerge when scaling A/B testing. The first is data bias, where training datasets fail to accurately represent the broader customer population. The second is test-cell leakage, where customers are unintentionally assigned to multiple experiments simultaneously. The third is short-term optimization that creates long-term harm, such as an AI model aggressively promoting a variation that increases immediate conversion rates but reduces customer lifetime value (CLV) or increases complaint volumes three to six months later.

According to Grant Thornton, AI model incidents in financial services are receiving increasing scrutiny from regulators across Europe and Asia. The solution is to design guardrails from the outset. Beyond conversion rates, every experiment should simultaneously monitor fraud rates, complaint rates, approval rates, dropout rates, and Net Promoter Score (NPS). If any metric exceeds predefined risk thresholds, the system should automatically pause the experiment and generate immediate alerts.

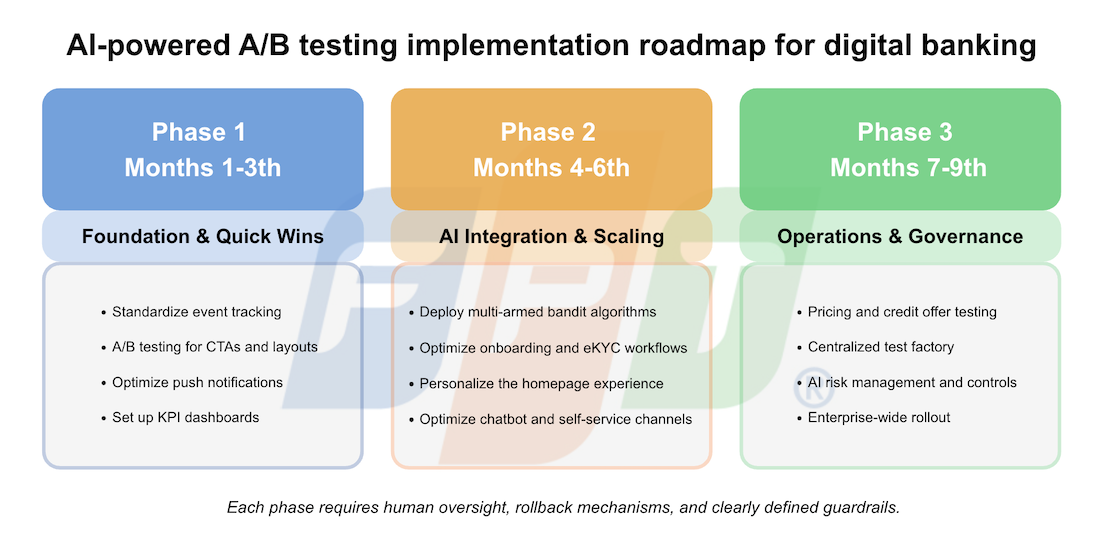

Implementation roadmap: Where should banks start?

The most common mistake is attempting to deploy the entire system at once. A more effective approach is to divide implementation into three phases, each lasting approximately three months.

Figure 3. 9-months roadmap for implementing A/B testing at scale in digital banking

Figure 3. 9-months roadmap for implementing A/B testing at scale in digital banking

The first phase focuses on building foundational capabilities and securing quick wins. This includes standardizing event tracking and conducting A/B tests on CTAs, layouts, content sequencing, and push notifications – use cases that are relatively low-risk and easy to measure. The second phase integrates AI capabilities and expands experimentation into onboarding, eKYC, homepage personalization, and chatbot optimization. The third phase transitions into governance-led operations by establishing a centralized “test factory,” where product, growth, data, and compliance teams jointly review hypotheses and institutionalize learning from experimentation. This phase also extends experimentation into pricing strategies and credit offers, with mandatory human-in-the-loop oversight.

A notable example is Singapore’s DBS Bank. The bank began building a centralized experimentation infrastructure in 2019 and, by 2022, was running more than 1,000 experiments annually, contributing directly to digital revenue growth. The key differentiator was not technology alone, but culture: every product decision was expected to be supported by experimental evidence rather than subjective opinions.

Conclusion: From experimentation to an optimization operating system

AI-powered A/B testing at scale is not a project with a defined endpoint. It is an operational capability that digital banks must develop as a long-term strategic advantage. It simultaneously delivers three major benefits: faster evidence-based decision-making, deeper personalization across customer segments, and lower experimentation costs through automated learning systems.

As Vietnam’s digital banking market continues to expand and competition intensifies from both traditional banks and fintech challengers, the ability to optimize customer experiences faster than competitors will become a critical determinant of market share over the next three to five years. The question is no longer whether banks should adopt AI-powered experimentation. The real questions are where to begin and how to implement it correctly.

A bank that learns from every customer interaction will always stay one step ahead, not because it employs more people, but because it operates a smarter system.

| Exclusive article by Mr. Luong Ngoc Binh – Digital Technology, Data & AI Expert in Banking and Financial Services

Mr. Binh is a financial services technology expert with 16 years of industry experience, including 10 years in digital banking. He specializes in Data and AI consulting for banking and financial institutions and has contributed to the development of core platform solutions for leading Vietnamese banks, including BIDV, Agribank, and PVcomBank. |

References

[1] Bluetext – AI-Powered A/B Testing: Smarter Experiments, Faster Results

[2] Stanford GSB – A/B Testing Gets an Upgrade in the Digital Age

[3] Tạp Chí Ngân Hàng – Ứng dụng AI tạo sinh tại các ngân hàng thương mại Việt Nam

[4] LaunchDarkly – Experimentation in Financial Services

[5] Grant Thornton – AI Banking: Risk, Regulation & Governance

[6] IBM Institute for Business Value – Banking in the AI Era